Brace yourself for this one!

Note from John Curry: This was taken from Jim McGreevy's site. I will give credit where credit is due and I thank Jim for calling this to our attention. What you see when you read the text below the chart is another example of what CORE member Judi Peaspanen called the "death spiral" of health insurance. [Note: I put the text first, then the chart. KBB] Looks like what some have said (that some at STRS wanted out of the health care business) might very well come true AND SOON! These potential increases are unconscionable. John

Friday, March 10, 2006

STRS Board Meeting: Preliminary Health Care Premium Estimates Hold Bad News

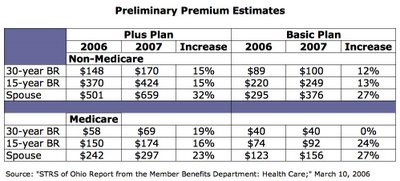

The Member Benefits Department presented their report on Health Care to the STRS Board on Friday, March 10, and the outlook for 2007 health care premiums was not good for benefit recipients. As shown in the chart above, premium increases may run as high as 32% over 2006 rates for non-Medicare spouses of members receiving benefits. The big jump results from the Board’s removal of the cap that was placed on 2006 rates to soften the transition to the higher rates that everyone knew were coming in 2006. Increases that year were held to 3% over 2005 rates. When that cap was adopted last year it was determined that it could only be a one-time event, a kind of “special subsidy” for health care for 2006.

It should be noted that these rate increases are preliminary estimates based on the claims data from 2004. The actual rates will be based on 2005 claims data, but no one expects the picture to be much brighter. Final rate schedules will be presented to the Board in August.

It is fair to say that the entire Board was suffering from “sticker shock” when this report was presented. Board members Mary Ann Flannagan, Stephen Buser, and Dennis Leone expressed distress at the size of the increases as did Vice Chair Conni Ramser who said “…we all understood in principle what would happen in 2007 when the 3% cap was removed, but the size of the increase is shocking.” Board member Judith Fisher pointed out that, although painful, the Board had no choice but to impose these rate changes if the Health Care Stabilization Fund (HCSF) was to be made more secure.

After considerable discussion the Board voted to authorize the STRS staff to proceed with preparations of a new premium schedule for 2007 based on actual 2005 claims data and no artificial cap on premium increases.

The financial hardship these increases will impose on many benefit recipients is their most obvious and disturbing aspect. However, if the higher premiums also cause “adverse selection” by STRS members (the practice of younger, healthier retirees finding cheaper insurance outside STRS leaving only older, less healthy members filing claims) then the financial health of the HCSF is further undermined, causing additional upward pressure on premiums. As this cycle is perpetuated, a health care benefit becomes more difficult to sustain. STRS health care coverage could ultimately price itself out of the market leaving benefit recipients to fend for themselves. In the long run this could prove to be an even greater burden for retirees than the increase in premiums that appears to be coming next year.

Article by Jim McGreevy

Friday, March 10, 2006

STRS Board Meeting: Preliminary Health Care Premium Estimates Hold Bad News

The Member Benefits Department presented their report on Health Care to the STRS Board on Friday, March 10, and the outlook for 2007 health care premiums was not good for benefit recipients. As shown in the chart above, premium increases may run as high as 32% over 2006 rates for non-Medicare spouses of members receiving benefits. The big jump results from the Board’s removal of the cap that was placed on 2006 rates to soften the transition to the higher rates that everyone knew were coming in 2006. Increases that year were held to 3% over 2005 rates. When that cap was adopted last year it was determined that it could only be a one-time event, a kind of “special subsidy” for health care for 2006.

It should be noted that these rate increases are preliminary estimates based on the claims data from 2004. The actual rates will be based on 2005 claims data, but no one expects the picture to be much brighter. Final rate schedules will be presented to the Board in August.

It is fair to say that the entire Board was suffering from “sticker shock” when this report was presented. Board members Mary Ann Flannagan, Stephen Buser, and Dennis Leone expressed distress at the size of the increases as did Vice Chair Conni Ramser who said “…we all understood in principle what would happen in 2007 when the 3% cap was removed, but the size of the increase is shocking.” Board member Judith Fisher pointed out that, although painful, the Board had no choice but to impose these rate changes if the Health Care Stabilization Fund (HCSF) was to be made more secure.

After considerable discussion the Board voted to authorize the STRS staff to proceed with preparations of a new premium schedule for 2007 based on actual 2005 claims data and no artificial cap on premium increases.

The financial hardship these increases will impose on many benefit recipients is their most obvious and disturbing aspect. However, if the higher premiums also cause “adverse selection” by STRS members (the practice of younger, healthier retirees finding cheaper insurance outside STRS leaving only older, less healthy members filing claims) then the financial health of the HCSF is further undermined, causing additional upward pressure on premiums. As this cycle is perpetuated, a health care benefit becomes more difficult to sustain. STRS health care coverage could ultimately price itself out of the market leaving benefit recipients to fend for themselves. In the long run this could prove to be an even greater burden for retirees than the increase in premiums that appears to be coming next year.

Article by Jim McGreevy

posted by Kathie Bracy at 10:39 PM

![]()

![]()

<< Home